Guide to S Corp taxes for small businesses

Key Takeaways

- An S Corporation is a tax classification that allows eligible businesses to use pass‑through taxation, meaning profits and losses flow to owners’ personal tax returns instead of being taxed at the corporate level.

- Businesses must meet strict IRS eligibility requirements to elect S Corp status, including having only U.S. individual shareholders, one class of stock, and no more than 100 shareholders.

- S Corporations must file Form 1120‑S and issue Schedule K‑1s to shareholders annually, generally by March 15. Then shareholders report their portion of income on their individual returns.

- S Corps may offer significant tax savings for some businesses when structured and maintained correctly. As a rule of thumb, if your company makes more than $40,000 in net profit, you may want to consider changing your tax status.

What is an S Corporation?

An S Corporation is an IRS tax classification that allows an eligible entity to be a pass-through entity for tax purposes. This means that the business owners will report the business profits and losses on their individual returns and pay any income tax.

Eligible entities are generally limited liability companies (LLCs) and corporations formed under state law.

To elect S Corporation status, the business must also meet the following eligibility criteria:

- Be a domestic (US-based) entity,

- Have only allowable shareholders,

- These are individuals, certain trusts, and estates

- They cannot be partnerships, sole proprietorships, corporations, or non-residents

- Have no more than 100 shareholders,

- Have only one class of stock

- Not be an ineligible corporation (i.e., certain financial institutions, insurance companies, and domestic international sales corporations)

If these requirements are met, you can make an S Corp election. If you’ve been in business a while, it’s also important to know that you can make a late S Corp election in some cases.

Now that we’ve established what businesses can elect S Corporation status let’s learn about S Corp taxes at the federal level.

Federal S Corp taxes – requirements

As mentioned above, an S Corporation’s profits and losses are passed through to its owners. This pass-through treatment means that the business generally won’t pay income tax on its profits at the federal level. That doesn’t mean that the business can ignore tax time, though, as there are still things that will need to be done.

Corporate-level taxes

Although S Corporations generally won’t have to pay income taxes, they are still required to file a tax return. The S Corporation does this by filing Form 1120-S, U.S. Income Tax Return for an S Corporation, by the deadline. The deadline for calendar-year S Corporations is generally March 15th. If your S Corporation has a fiscal tax year the deadline will be the 15th day of the third month following the last day of the business’ tax year. If the business cannot complete and file Form 1120-S by the deadline it can request a 6-month extension by filing Form 7004, Application for Automatic Extension of Time To File Certain Business Income Tax. Note that, as always, deadlines that fall on weekends or holidays will shift to the next business day.

Part of the process of completing Form 1120-S is to complete a Schedule K-1, Shareholder’s Share of Income, Deductions, Credits, etc., for each shareholder. The Schedule K-1 will tell the shareholders/members the items that they will report on their individual returns. The schedules must be issued to the shareholders by March 15th for calendar year S Corporations unless an extension is filed.

One thing to note is that if an S Corporation has certain built-in gains or passive income at the corporate level, it may be required to pay income taxes. There is a section of Form 1120-S where these items are reported. Form 1120-S is generally referred to as an information document since it reports information to the IRS and shareholders/members. Let’s shift gears and discuss what shareholders do with this information.

Shareholder-level taxes

We have mentioned a few times that shareholders will pay income tax on the profits of the S Corporation, but we haven’t talked about how that is done. The first thing a shareholder needs to do is ensure that they receive a Schedule K-1 from the business. It is important to follow up with the business if the shareholder did not receive a Schedule K-1 since they will need it to complete their individual tax return. If the business filed for an extension, the shareholders may also need to request a filing extension.

Once shareholders receive their Schedule K-1 they will report that information on Schedule E, Supplemental Income and Loss, of their individual return. The income each shareholder reports on their individual return is taxed at their individual tax rate. This is in contrast to a C Corporation, which pays a flat tax rate of 21%.

Cash distributions to an S Corporation shareholder are generally tax-free since shareholders pay tax on their share of the business’ income. C corporation shareholders don’t enjoy this benefit – they pay taxes on any dividends they receive.

Shareholders should keep track of their basis in stock and debt on a continual basis. Cash distributions to shareholders are only tax-free to the extent of stock basis. Shareholders should use Form 7203, S Corporation Shareholder Stock and Debt Basis Limitations, to keep track of the basis. This form doesn’t always need to be filed with the IRS, but it is good practice to fill it out and keep it with your records.

Estimated payments

Since the business generally doesn’t have to pay income taxes, estimated payments usually aren’t required. Shareholders, on the other hand, may be required to make estimated payments based on the tax they expect to owe. Each shareholder should communicate with the business throughout the year to estimate their share of income each quarter to determine if estimated payments are needed.

Federal employment taxes

Changing your structure may save you thousands.

Use our online tool to find out how much you could be saving.

S Corporations that have employees will need to withhold, deposit, and pay employment taxes. These S Corp taxes include income tax withholding, the employer and employee share of Social Security and Medicare tax (FICA), and unemployment tax (FUTA). These taxes must be deposited throughout the year, and the due dates depend on the tax liability from the prior years and the type of employment tax return the corporation files.

Most S Corporations will be required to file Form 941, Employer’s Quarterly Federal Tax Return, on a quarterly basis. The business will also need to file Form 940, Employer’s Annual Federal Unemployment Tax Return annually.

Paying owners

Shareholders who provide services to the business will also need to be paid a reasonable salary for their work. There is no test for what constitutes a reasonable salary, but some factors to consider are:

- What would an employee performing the services be paid?

- What is the financial condition of the business?

- What credentials does the shareholder have?

- How many hours does the shareholder work?

This is not an exhaustive list, and you should consult a tax professional when determining a salary for the shareholder. The business will need to account for employment taxes for the shareholder as if they were any other employee.

There are few S Corp tax benefits that come with paying shareholders that provide services, the first being that the compensation will be deductible on the business’ Form 1120-S. Also, if the company pays insurance premiums on behalf of the shareholder providing services, the company may be able to deduct premiums. Additionally, the shareholder may be able to claim the self-employed health insurance deduction (SEHID) for those premiums if certain requirements are met.

Another perk for the shareholder is that they will get credit for social security taxes paid on their wages. While the shareholder’s wages are subject to employment taxes, the remaining share of the shareholder’s income will not be subject to self-employment tax. These perks for the shareholder and business as mentioned above, can be attractive to shareholders considering working in the business.

State S Corp taxes – requirements

As we mentioned above, the S Corporation designation is a federal income tax classification. Most states recognize a business’ federal S Corp election – in these states, business is a pass-through entity for state tax purposes as well. This is not the case for all states though, and some states still impose a corporate income tax on S Corporations. Since every state is different, it is important that you consult the rules for the state or states that you are organized in and the ones you do business in, as they may treat the S Corporation differently.

In addition to income taxes, states may impose other taxes such as employment, gross receipts, or franchise taxes. These taxes will typically have a corresponding form and due date that can be different from the federal due dates discussed above.

While we have covered a lot of ground concerning S Corp taxes, you may still have questions. A Block Advisors Small Business Certified tax pro can help you understand the nuances of your state’s tax requirements.

Get expert tax prep at an affordable price

Don’t wait to file your S Corp taxes.

Does an S Corp really save on taxes?

Depending on your circumstances, yes, it is possible to save money as an S Corporation. Business owners who are currently reporting income as an LLC or Sole Proprietor may be able to reduce their tax burden by filing taxes as an LLC with an S Corp election. The savings come from profits no longer being subject to self-employment tax. Additionally, shareholders who pay themselves a reasonable salary only pay employment taxes on the salary portion of their income. They are then able to take the remaining profits of the business as a cash distribution, which again is not subject to self-employment taxes.

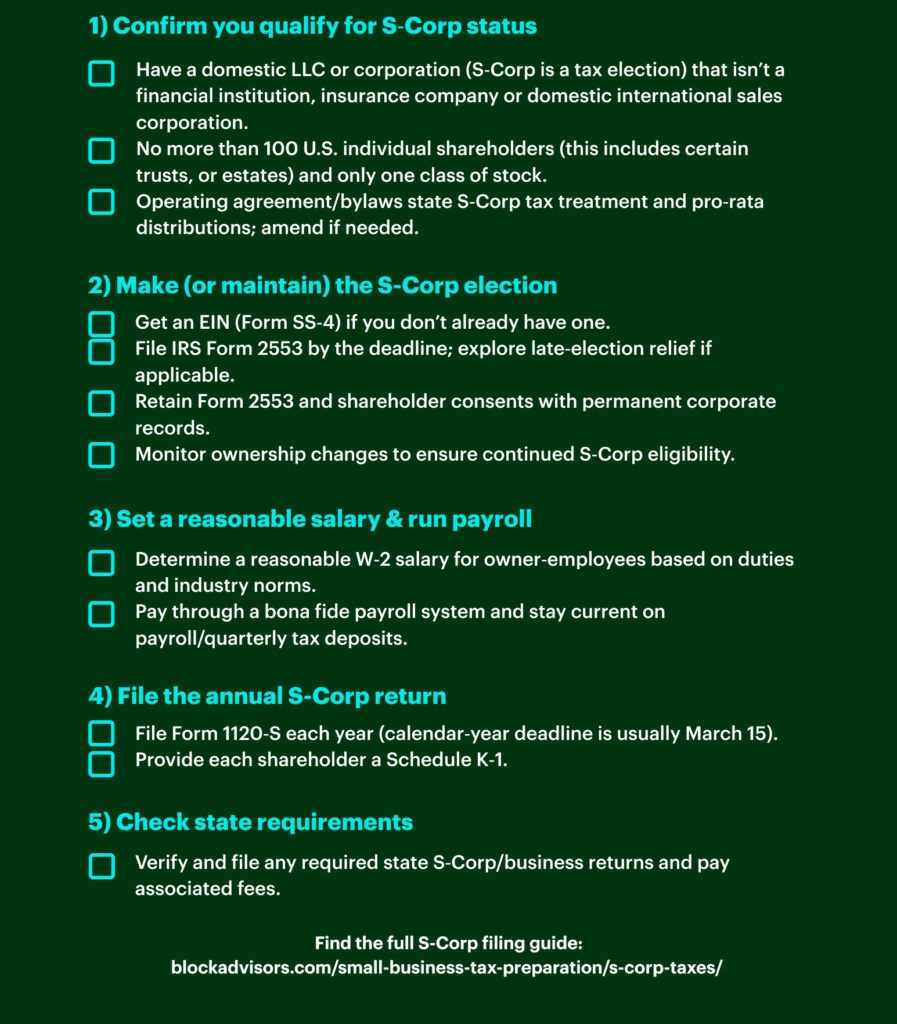

S corporation tax checklist

Managing an S Corporation comes with unique tax responsibilities that business owners must navigate carefully to maintain compliance and maximize possible benefits. Unlike C Corporations, S Corps offer pass-through taxation that can provide significant tax advantages, but only when properly structured and maintained. To help you stay on track throughout the year, you may want to compile an S Corp tax checklist.

What should be included in an S Corp tax checklist?

If you’re asking, “What should be included in an S Corp tax checklist?” keep reading. Below is Block Advisors’ S Corp tax checklist. It covers critical tasks every S Corp owner should be mindful of. Whether you’re establishing your S Corp for the first time or maintaining an existing S corporation election, following the S corp tax checklist steps below will help ensure you meet IRS requirements while optimizing your tax position.

The Domestic LLC or Corporation electing S Corp tax status must:

- Confirm S Corp status eligibility

- Can’t be a financial institution, insurance company, or domestic international sales corporation.

- Can have no more than 100 U.S. individual shareholders, including certain trusts and estates, and only one class of stock.

- Must have an operating agreement or bylaws that state S-corp tax treatment and pro-rata distributions.

- Make or maintain the S Corp election

- Secure an EIN (Employer Identification Number) using Form SS-4

- File IRS Form 2553 by the tax deadline. You may also be able to take the S corp election late in some situations.

- Keep Form 2553 and shareholder consents in your permanent corporate records

- Track ownership changes and monitor future S Corp eligbility

- Pay a reasonable salary & run payroll

- Set a reasonable W-2 salary for owner-employees based on responsibilities and industry benchmarks

- Utilize a bona fide payroll system to distribute salaries and stay current on payroll and quarterly tax deposits.

- Complete annual S Corp tax return

- File Form 1120-S each year by the S corp deadline – generally, March 15.

- Send a Schedule K-1 form to each shareholder

- Follow state requirements

- Ensure you’re adhering to your individual state’s filing requirements for S-corporations and pay any state-level fees, if applicable.

Printable S Corp checklist

Where can businesses get help using an S Corp tax checklist?

Filing your S Corp taxes right can feel complicated. Each business owner’s situation impacts potential savings and there are a lot of details to keep track of. Many business owners find that working with an experienced professional can help them feel more confident as they go through their S Corp tax checklist.

Block Advisors Small Business Certified tax pros have your back to help you understand S Corp elections and how to navigate S corp taxes. Make an appointment today.

S Corp Taxes Frequently Asked Questions

Q: What rate is an S Corp taxed at?

A: An S Corp benefits from pass-through taxation, so the S Corp generally does not pay income tax directly. Income tax is reported by each shareholder on their individual return and is taxed at their individual tax rate.

Q: Is an S Corp taxed at 21%?

A: No, an S Corp typically does not pay income tax directly. Rather, income is passed through to shareholders who pay income tax on their individual tax returns. C Corporations, which are different from S Corps, have a flat tax rate of 21% paid by the corporation.

Q: What are the tax advantages of an S Corp?

A: Pass-through taxation is the primary tax benefit of an S Corp. This means that business owners will report the business profits and losses on their individual returns and pay any income tax. The S Corp itself usually does not pay taxes. Typically, the S Corp will need to pay owners/shareholders that provide services a reasonable salary to maximize savings potential. Additionally, a secondary benefit is that each owner’s share of the S corporation’s income isn’t subject to self-employment tax. Depending on each individual’s tax situation, these benefits can result in substantial tax savings.

About the Author

Carl Breedlove is a Lead Tax Research Analyst at The Tax Institute, H&R Block and Block Advisors’ center of tax expertise. He specializes in small business, rental property, and state taxation. Carl is a graduate of the University of Missouri-Kansas City School of Law with Master of Laws (LLM) and Juris Doctor (JD) degrees.

This article is for informational purposes only and should not be construed as legal advice. You may want to seek the advice of an attorney to evaluate all relevant considerations.